REIT Total Return Portfolio Heading into the 2nd half of 2022

We view investing as a constant measure of worth against opportunity cost. The opportunity cost consists of the next best opportunity and is always in flux. In times like today when the entire market has sold off, opportunity cost is high because so many investments are cheap. As such, the criteria for inclusion in the portfolio are more stringent than normal.

Having a pre-existing gain or loss in a stock is irrelevant to its going forward returns and should only be considered with regard to taxation. In investing the 2nd Market Capital Total Return Portfolio we are careful to neither fall in love with winners nor get mad at losers. Each stock is continuously reassessed – its forward expected returns versus its opportunity cost.

It is by this method that we keep it perpetually invested in whatever is most opportunistic today. Tomorrow is a new day and tomorrow it will be invested in whatever is most opportunistic then. With updates of this nature, it cannot get stale and its performance is just a matter of whether we are right or wrong about the forward returns of the stocks within the portfolio.

We believe there are a few key advantages to the particular group of stocks selected

- The average stock in the portfolio is trading at 82% of net asset value. Getting properties at a discount to their private market value enhances the cashflow return on each dollar invested.

- $159,295 in market value is generating $13,296 in FFO annually. That is an FFO yield of 8.3%.

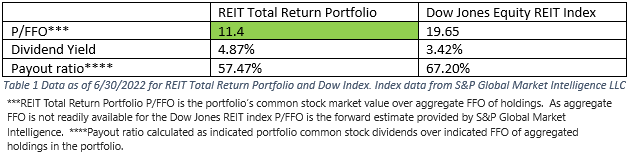

- The dividend yield, while high at 4.87% is only just over half of the FFO yield allowing these companies to retain a substantial amount of cashflow for growth. Retained cashflow is of particular importance at times like this when the market being cheap makes equity issuance prohibitively expensive.

We believe this stacks up quite favorably against the REIT index. P/FFO of the portfolio is much lower at 11.4X compared to 19.65X for the REIT index.

We do not blindly buy value for the sake of value, but rather achieved the value through a combination of buying stocks that are undervalued and avoiding those that are overvalued. In this way, we can achieve similar or better fundamental growth rates, but at a higher going in yield.

Diversification

While focused on bottom-up individual stock selection we do intentionally maintain diversification with overweights in the property sectors that are beneficiaries of the macro environment and underweights in sectors plagued by oversupply.

There is nothing special about our assessment that office is a bad sector. It is an overwhelming consensus that office, particularly that in oversupplied coastal cities, is hurting. However, the phenomenon of index-based investing which is now about 50% of the total market is that it still buys the junky stuff even if it is known to be junky.

So, while active managers like us are already mostly out of office, the index ETFs are still buying office for one simple reason – the office REITs are big.

A few areas in which we are substantially overweight relative to the index are

- Land – 12.2% vs almost none in the index

- Manufactured housing – 6.65% vs ~1% in the index

- Casinos – 5.87% vs almost none in the index

Performance

We began trading the REIT Total Return Portfolio on 7/1/16 with $100,000. No capital has been added or removed since allowing for clean tracking of performance.

The 6 years in which 2CHYP has been open have been quite a rough period for the market with the COVID crash and now the Fed-driven or recession-fearing crash of the present. Careful stock selection and constantly watching for opportunities to pivot into superior opportunities have helped us outperform the index.

Since its inception on 7/1/16, our REIT Total Return Portfolio has returned 50.02% while the REIT index (RMS) has returned 27.02%.

Wrapping it up

We will continue to analyze the REIT universe in the face of a rapidly evolving macro environment. As things change and prices move new opportunities arise. We have every intention to capture them.

Evolving economies create opportunity

Our REIT Total Return Portfolio is actively managed to pivot into wherever the opportunity is greatest. We are now offering portfolio mirroring in which the trades in our REIT Total Return Portfolio are automatically executed in client portfolios simultaneously and at the same price.

Important Notes and Disclosure

Material Market and Economic Conditions. March 2022-2023: Significant increases in the Federal Funds Rate by the Federal Reserve have caused REIT market prices to decline more than the broader markets. REITs rely on debt financing to acquire properties and fund their operations; expiring lower-cost debt is being refinanced at higher interest rates due to prevailing market conditions. March 2020: REIT Total Return’s value declined substantially as COVID shut down the economy. It recovered in 2021 as the economy reopened. January 2019: Tax-loss selling’s calendar expired and the government reopened on January 25, 2019. The combined effect caused our shares to rise more than the broader markets. December 2018: Another Fed-Funds rate hike, unresolved US-Chinese trade, a partial government shutdown, and an exaggerated tax-loss selling season put extreme downward pressure on equity prices. All of these factors contributed to diminished liquidity and more significant share price declines in small-cap/value issues; REIT Total Return is focused on small-cap/value issues, so our decline was significantly more precipitous.

Material Conditions, Objectives, and Investment Strategies. REIT Total Return is an actively managed investment portfolio of real estate equities, primarily common and preferred shares of REITs, with an aim to generate high total returns from a mix of dividends and capital appreciation.

All REIT Total Return Portfolio performance information on this page is based on the performance of the Portfolio Manager’s account, using the manager’s own funds. Performance of the Portfolio Manager's account is calculated by Interactive Broker on a daily time-weighted basis, including cash, dividends and earnings distributions, and reflects the deduction of broker commissions (when commissions were charged). Actual client returns will differ. **2nd Market Capital’s advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

None of the performance information displayed on this page is based on the actual performance of any 2MCAC client account investing in this portfolio. The performance in a 2MCAC client account investing in this portfolio may differ (i.e., be lower or higher) from the performance of the account managing this portfolio and portrayed on this page based on a variety of factors, such as trading restrictions imposed by the client (resulting in different account holdings), time of initial investment, amount of investment, frequency and size of cash flows in and out of the client account, applicable brokerage commissions (when commissions were charged), and different corporate actions. Clients investing in this portfolio may view the actual performance of their investment in this portfolio by logging into their Interactive Brokers account and reviewing their customized dashboard.

Clients may restrict any of the securities traded in their account but should note that any restrictions they place on their investments could affect the performance of their account leading it to perform differently, worse or better, than (a) the above-portrayed account or (b) other client accounts invested in the same portfolio.

Forward-looking statements. Commentary may contain forward-looking statements which are by definition uncertain. Actual results may differ materially from our forecasts or estimations, and 2MCAC cannot be held liable for the use of and reliance upon the opinions, estimates, forecasts, and findings in these documents.

Past performance does not guarantee future results. Investing in publicly held securities is speculative and involves risk, including the possible loss of principal. Historical returns should not be used as the primary basis for investment decisions. Although the statements of fact and data in this commentary have been obtained from sources believed to be reliable, 2MCAC does not guarantee their accuracy and assumes no liability or responsibility for any omissions/errors.

Use of Leverage or Margin. REIT Total Return Portfolio will utilize margin only for trading purposes (the ability to use the proceeds from stock sales immediately for new purchases instead of waiting for settlement), but not for borrowing purposes.

Benchmark Comparison. Our REIT Total Return Portfolio is compared to the Dow Jones Equity REIT Index and the MSCI U.S. REIT index because they are common REIT Indices. The Dow Jones Equity All REIT Index is designed to measure all publicly traded equity real estate investment trusts (REITs) in the Dow Jones U.S. stock universe. The MSCI US REIT Index is comprised of equity real estate investment trusts (REITs) eligible included within the eight Equity REIT Sub-Industries of the Equity Real Estate Investment Trust (REITs) Industry. It is not possible to invest directly in the Dow Jones Equity All REIT Index or MSCI US REIT index. Index returns do not represent the results of actual trading of investible assets/securities. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the securities underlying the index. The imposition of these fees and charges would cause the actual performance of the securities to be lower than the Index performance shown. The results portrayed include dividend income. Our REIT Total Return Portfolio may include REITs that are not eligible for inclusion in the Dow Jones Equity All REIT Index or MSCI US REIT Index.

There can be no assurance that a benchmark will remain appropriate over time and 2MCAC will periodically review the benchmark’s appropriateness and decide to use other benchmarks if appropriate.

Expenses. Returns reflect the deduction of any transaction expenses. REIT Total Return's advisory fees are simulated and applied retroactively to present the portfolio return “net-of-fees”.

Calculation Methodology. Returns are calculated by 2MC with data from Interactive Brokers LLC using the Modified Dietz method, a time-weighted measure of performance in which cash flows are weighted based on their timing. Dividends in REIT Total Return are reinvested.

S&P Global Market Intelligence LLC. Contains copyrighted material distributed under license from S&P.